Now that’s what I call an Investible Pipeline of Infrastructure Projects in the regions (Volume 1)

Involved in regional economic development? Then you won’t be able to move for the phrase ‘investible pipeline’ – a series of ‘investment-ready’ infrastructure projects seeking private and public investment to turn regional leaders’ policy aspirations into tangible economic output.

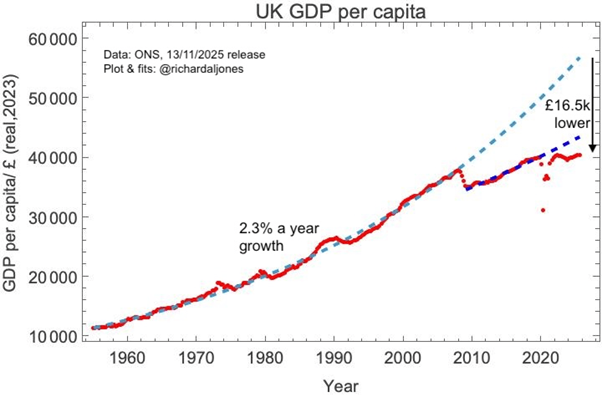

The stakes are enormous. As the brilliant Richard Jones continues to emphasise via his Softmachines blog, UK output - measured as GDP per capita - has been woeful since 2008 (see graph below). Crucially, the public finances continue to worsen – with the OBR recording a £138bn deficit in state receipts vs. spend in 2025/26. At the same point as there being less to go round, a host of industries and companies are seeking financial help to secure profitability – witness for example grant investments in housebuilding to overcome viability challenges, or regional grants being applied to support inward investment in aerospace, automotive or the low-carbon energy supply chain. In our heads, there’s a virtuous venn diagram covering public investment, private investment and ‘ready’ projects to deliver increased growth and to improve the UK’s position in the world.

Awful since 2008

The need for every region in the UK to have these robust ‘public-private’ project pipelines for new infrastructure - with clear evidence of business cases, delivery plans and risk assessments in situ – have received a further kick in recent months: the ongoing (and growing, as per the Chancellor’s recent Mais lecture) devolution of powers to regionally elected Mayors, emphasising their role at the forefront of growth; alongside the reintroduction of regional Spatial Development Strategies.

Oh – and let’s not forget another major motivating factor: capital needing to find a home in projects that deliver both absolute and social returns. We’ve previously covered how Mansion House Accord signatories, including pooled local government pension funds, are seeking opportunities that fall well within this scope:

Signatories to the Accord will pledge to invest 10 percent of their workplace portfolios in assets that boost the economy such as infrastructure, property and private equity by 2030. At least 5 percent of these portfolios will be ringfenced for the UK, expected to release £25 billion directly into the UK economy by 2030.

Match that with increased Central Government funding commitments to the regions in recent weeks and further planned investment from the likes of Legal & General and Aviva, then there’s an awful lot riding on the quality of these pipelines.

So what should they include? This report looks at three related elements:

What private investors are looking for from projects within these pipelines;

Our ideas on what projects should be brought forward and ‘sponsored’ within regional infrastructure pipelines across the UK; and

Regardless of pipeline development, a huge need remains for the public sector to act as funder of last resort to support the delivery of ‘high IP’ infrastructure projects that would not qualify as ‘investment ready’.

Our role in this is two-fold: brokering private projects into these investment pipelines, prior to working up the business cases to secure and ultimately use this funding to accelerate regional growth across the UK. If you have a project that fits this bill or want to discuss any of this report further, get in touch with us.

What regional investible pipelines should look like

Having looked at the current status of pipelines across the UK, it is already clear which region is head and shoulders in the way pipelines are both arrived at and presented: yes Ladies and Gentlemen, it’s Greater Manchester – and there’s lots for other regions to learn from.

This is not especially surprising; Greater Manchester of course was already a forerunner in regional spatial development (through its Places for Everyone plan) as well as having a mature public-private investment partnership, which I saw first-hand in Greater Manchester Investment Fund monies supporting the build-out of Logistics North in Bolton in the last decade. What is particularly pleasing though is:

How simply and clearly each of the projects is explained, linked to the region’s strengths, the UK’s principal economic mission and what the investment opportunity actually is; alongside

How well it is spatially presented.

This pipeline has undoubtedly influenced the well-documented increased flow of private capital entering the region in tandem with public investment, through its projects offering the required development return AND being suitably de-risked to invest in. Crucially, it’s also supported a growing number of actors becoming involved in the development of new interventions and projects; witness CBRE and Bradshaw Advisory’s work over the past two years in exploring how ‘public authorities could intervene with innovative capital products that sit between debt and grant. under the Subsidy Act 2022’, principally in accelerating commercial development to come forward.

The end result is instructive for the UK’s future economic success and for what other regions bring forward within their own pipelines. From 2015 to the 2023, Greater Manchester was the UK’s fastest growing sub-regional (i.e. ITL2) economy in this latter period, growing at double the rate of the UK (GM: 3.1% per year; UK: 1.5%); this included it growing more quickly than the UK economy in seven of those nine years to 2023. It propelled the region to new economic heights, with the most recent data showing that GM’s economy now stands at north of £100bn for the very first time.

In short, the approach worked – and we think it worked (in part) to Greater Manchester spending time answering the right question: what are investors looking for exactly?

What are private infrastructure investors looking for?

A great place to start on this is The Good Economy’s (“TGE”) recent ‘Deep Dive Webinar’ on what private investors in infrastructure are looking for. Held to emphasise the principal conclusions of TGE’s excellent white paper on investment in the infrastructure sector, we consider it to be essential listening as it got to the foundations of why private investment does or does not happen.

Two things are absolutely fundamental here. The first is the predictability and size of the investment return from the project; the second is how well risks relating to the project are known, understood and mitigated. If you listen to some of the opinions within the report or podcast, two overriding investment types come to the fore – either:

A PFI type model where the private institution pays for the upfront infrastructure, in return for index-linked long-term repayments from public institutions; or

Where private investment provides the majority of upfront investment, with secondary funding coming from public institutions to assure an overall level of return above the investors’ required hurdle rate.

Our ideas on what sort of future projects should be brought forward within future regional pipelines

With these two investment outcomes in mind – where neither public or private investment would happen without the other - we’re particularly keen to see four types of infrastructure investment made across UK regions as part of their future investment pipelines to help address the UK’s chronic productivity problem. This list is certainly not exhaustive but they are the issues that keep our founder up at night…..

HOUSING

There’s a huge call for Housing investment, given that it is extremely unlikely we’ll get near the Government’s target of delivering 1.5m new homes in England by Summer 2029. We think investment attention should fall on two main areas, with the state ‘topping up’ schemes that are majority privately funded.

The first idea is for the state – either Homes England, a Combined Authority, a Local Authority or even a ‘local place partnership’ – to create a Regional Sovereign Wealth Fund aimed at SME housebuilders. This idea – which we explored with Sky-House Co – involves the state buying a small number of properties at the end of a development to provide the capital for a developer to move onto their next development and for the state to secure long-term rental income. We made the following assumptions based on a final phase of 10 homes at the end of an indicative 45 home scheme in Sheffield:

The completed homes have an asset value of £1.75m. To hold these properties unsold would cost the SME a further £120,000 in finance costs, thus eroding development profit and further affecting cashflow. This creates a vicious cycle: with no cash to fund planning costs for the next project (assumed to be another £150,000), sites inevitably stall.

A Sovereign Housing Fund could take these final unsold homes with a 5-10% discount, which we assumed a value of £1.6 million. Whilst this would mean the SME exiting the development with £1m of profit instead of £1.2m, it would immediately remove £120,000 of finance costs and create the cashflow to move onto its next development, accelerating the build out of sites from SME efforts and increasing spend with the supply chain.

The return for the public sector is also attractive. The fund could then offer these homes for market rent, which could – in theory – achieve an estimated £125,000 rent roll (estimate) at a 7% yield. If the acquisition was funded through the use of money at ‘Government rates’ (at c. 4.5% rates), debt would be c.£65k pa with income of £125k pa – providing a £60,000 profit per annum. If inflation is assumed at 2% (we know this is ambitious!) to calculate long-term house price growth, the ten rental properties would be worth c.£2.135m in ten years, providing a further £385,000 of value growth to the UK plc balance sheet.

The second idea is for the Government’s Brownfield Housing Funds (BHF) applied across several regions to be widened to include greenfield land to ramp up serviced land delivery. Mayoral regions such as East Midlands and South Yorkshire have done an extremely good job in spending their 2024 and 2025 BHF allocations on early stage interventions, for example demolition and remediation works, to support Housebuilders/master developers to generate acceptable returns on difficult sites. (Here is an example of a grant we’ve recently secured for a leading SME housebuilder in the North of England).

Governance processes are now clearly established for application sifting, due diligence and eventual Investment Committee decision making in these regions; a number however face a dwindling brownfield land supply for residential in certain Boroughs. A wider fund to increase site eligibility could therefore make a material difference to regional housing starts. In our view, this ought to include a dedicated percentage towards SME housebuilders, providing more support to them in what has been a particularly difficult market in recent months.

COMMERCIAL DEVELOPMENT

As Greater Manchester has demonstrated, CAs can help address the chasm between investors and commercial occupiers through products that sit somewhere between traditional grants and loans to accelerate new commercial space build-out and to support the scale-up of some of the UK’s brightest new businesses, while providing a steady and predictable development return. This could take two forms:

One option could include a region’s Mayoral Combined Authority acting as ‘rent guarantor’ on new units in specific growth locations linked to either its previously stated spatial or sector priorities. Many years ago whilst at Harworth Group, I worked with Barnsley Council in them taking this intervention via its Property Investment Fund; read more on its results here.

The commercial case sees the MCA paying a slightly lower than expected market rent to a developer to support build out in the first place through it’s ‘.gov.uk’ status; the benefit to the taxpayer would be through both a rent ‘profit’ on the sub-lease plus the business rates garnered.

The profit can then be reinvested into the programme itself – thereby becoming self-sustaining – or could be ported to other Mayoral priorities.

Alternatively:

‘’Gap financing’ could be applied to overcome initial site hurdles for key commercial developments – including for remediation and infrastructure.

Whilst the era of ‘major grant schemes’ for commercial developments is over, creating ‘soft loan’ terms for developers – on lower rates than that offered by banks – would provide both a return to the state as well as reducing the cost of development. The West Midlands does this particularly well, offering Senior Debt, Mezzanine Debt or Equity Investment alongside the capacity for ‘co-investment’.

This could also be applied to a variety of other use cases, including renewables, building refurbishment (given the Government‘s wish for all commercial buildings to be EPC ‘C’ by 2027) and leisure uses in city centres to support their residential densification.

ENERGY INFRASTRUCTURE

TGE’s deep dive report included a major section on previous investments made by Equitix - a leading small to medium mid-market investor, developer, and fund manager of infrastructure assets, managing over c.£14.9 billion across more than 300 projects in 24 countries. Equitix have made equity investments into companies within energy sub-sectors as diverse as Energy-from-Waste and Battery Energy Storage Systems (BESS)….but what potential investments within regional infrastructure pipelines?

Given the desire for stable long-term income, this could take the form of direct intervention in projects such as District Heating, harnessing waste heat from industrial facilities. Too few District Heating programmes are coming forward in the UK, in part due to the additional ‘upfront’ infrastructure required to harness it – including in building ‘energy centres’. If a ‘PFI’ model is applied, investors could provide the upfront capital for this infrastructure in return for an income from the offtaker. This income of course would need to be less than what the offtaker is saving in making the move to district heating in the first place…..

SUPPORTING KEY LOCAL COMPANIES WITH AN ESTABLISHED ‘ADVANTAGE’

Finally, we’re aware of a number of live examples where UK companies with strong IP - particularly those in manufacturing and its supply chain – require capital investment to ramp up speed of production, or to significantly reduce the cost or weight of their products.

These projects – with the public and private sector going in side by side as capital investors to support companies to increase production, recruit new roles and ultimately increase their profitability – can repay this initial capital contribution through the latter. One recent Rotherham-based manufacturing example – where a bank loan was followed by a grant/loan from South Yorkshire MCA – can be found here.

BUT……..KEEP LOOKING TO THE FUTURE

The big issue with these ideas of course is that they are rooted in our current economic environment in 2026….and that the economy is rapidly evolving. David Richards’ excellent ‘Sunday Signal’ series has regularly emphasised how AI and machine learning are rewriting industrial rules, reflecting here on a recent study by those Donald Trump fans at Anthropic. It creates huge opportunities, yet could fundamentally restructure huge swathes of our industrial fabric.

Our future infrastructure pipeline in ten, twenty, thirty years’ time could look very different indeed. AI, climate pressure, ‘virtualisation’ and the further ageing of the population will change the nature of the economic challenge – creating new value chains in future decades that will feel as ordinary as e-commerce and mobile apps, revolutionary 25 years ago, feel now.

How quickly can the state and investors flex for these future challenges? That’s one for a future report.

Going beyond pipelines: the need for the state to invest as ‘funder of last resort’

The final part of this report doesn’t actually relate to regional infrastructure pipelines at all; it reflects on the need for the state to continue its role as ‘funder of last resort’ to intervene on high IP projects that ordinarily would not qualify as ‘investment ready’.

Back to that man Professor Richard Jones again. He’s one of the few to talk about one of the most exciting, and scientifically curious, projects in the UK in recent weeks – the Spherical Tokamak for Energy Production (STEP) nuclear fusion programme in Bassetlaw (East Midlands). His superb blog sums it up as follows:

The UK government has a very ambitious plan for nuclear fusion, which I don’t think is widely enough known about. The plan is to build a pilot nuclear fusion plant able to deliver electrical power to the grid by 2040 – the Spherical Tokamak for Energy Production (STEP). The project was launched in 2019, and the current government has guaranteed funding for it at the very significant level of £500m a year for five years.

It has a high profile fan in the Secretary of State for Energy Security & Net Zero, who gauges it as a future source of limitless clean energy; he also believes, as we do, that the UK is a world-leader in this technology.

The problem? There are number of problems to be overcome to realise its potential in practice – particularly in relation to material technology – which Professor Jones’ blog does an admirable job in summarising. Everything needed for STEP to work is possible in principle, but nothing is easy, and success is far from guaranteed.

Bringing it back to this report, no private investment committee in the world would commit to it….but we agree with Richard – the UK should do it anyway. Solving its engineering and technical challenge is exactly the type of huge challenge which the UK used to pride itself in – one that could fundamentally change how we all live and work. Richard sums it up far better than I ever could here:

STEP is a really substantial engineering project that will build project capacity and drive much research and development, and build innovation capacity, in areas like materials science, robotics, and large scale computer modelling, here in the UK. We are already seeing a cluster of private sector fusion companies growing up near the UKAEA headquarters in Culham, attracted by the skilled people and the climate of innovation in related areas of technology.

The location of STEP in West Burton should significantly broaden the geographical impact of UKAEA. The location is in commuting distance of Doncaster, Scunthorpe and Sheffield, communities that are still struggling with the impact of deindustrialisation, but which are building new capabilities in advanced manufacturing.

Why is this relevant? Because there are lots of other deserving high IP cases across the regions that would fail the investment test today but may ‘pay big’ in future. Fiscal responsibility means that leadership in our regions cannot select many to support – but projects like these, where the effect on the supply chain, on future skills development and ultimately our place in the world – should be. Keep thinking big.

Get in touch

As ever, get in touch with us on any part of this report, including scheme promotion or in working up business cases (and supporting documentation) to secure the finances needed to accelerate their build-out.

And finally….

It wouldn’t be a Bellona report without some form of delve into the archive – in this case showing what some believed the future to be back in 1985.

Yes folks, it’s the Sinclair C5. Would you have supported investment into the tooling required to build these 5mph transport marvels at scale? It’s now heralded as one of Britain’s most iconic white elephants, and you can pick one of these up in Letchworth’s shop of curiosities for a cool £4,000…..